Marina One's $1,702 psf Record Low: What It Tells You About CCR Value

A record low at Marina Bay made headlines this week. The number is the easiest part of the story — the harder part is what it means, and for whom.

The short read

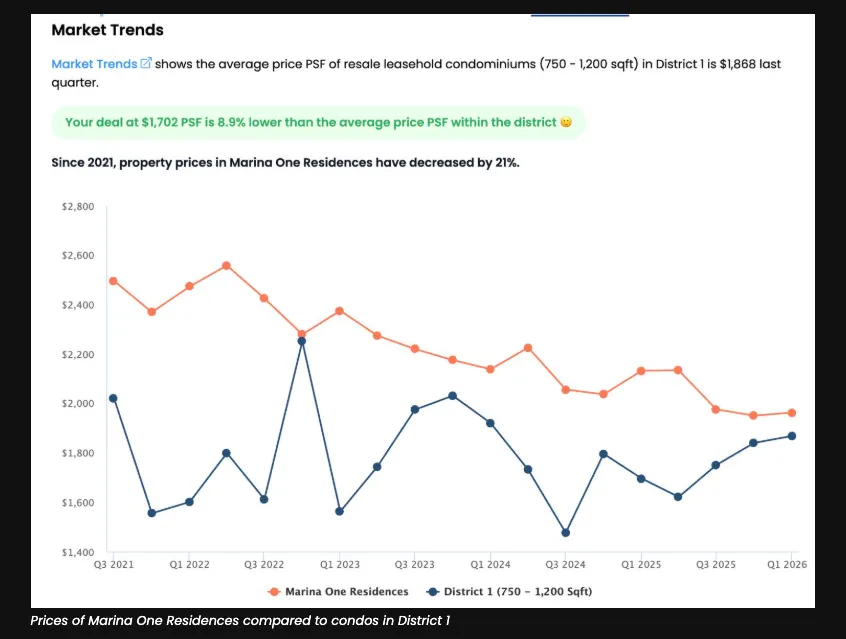

A 764 sq ft one-bedder at Marina One Residences sold for S$1.3 million, or $1,702 psf — a record low for the development, 12.4% below its own 12-month average and 8.9% below the District 1 resale average. The seller, who bought in April 2021 at $1,943 psf, exited with a $185,000 loss.

One transaction is not a market. Across five cycles I've seen new lows become floors, and new lows become the first step down — and the honest answer is we don't know yet which this is. Watch sub-sale volume and rental absorption over the next two quarters. For most families buying a ten-year home, this print changes nothing; the quieter opportunity sits with right-sizers weighing a compact CBD chapter.

A one-bedroom unit at Marina One Residences changed hands on 28 May for S$1.3 million, or $1,702 psf — a new psf low for the entire 1,042-unit development, as EdgeProp reported this week. The unit is a 764 sq ft one-bedder on the eighth floor, a regular layout with a balcony, in one of the most architecturally ambitious residential addresses in the CBD.

The seller did not do well. They bought the unit in April 2021 at $1,943 psf and exited five years later at $1,702 psf — a loss of $185,000 over roughly 5.1 years, or an annualised loss of 2.6% before transaction and financing costs.

I’ve watched the CBD reprice three times since 2009. The headline — a record low at a marquee Marina Bay address — is the easiest part of this story. The harder part is what it means, and for whom.

What actually happened, in context

Start with where $1,702 psf sits. It is 12.4% below Marina One’s own 12-month average of $1,943 psf, and 8.9% below the District 1 average for resale leasehold condos of 750 to 1,200 sq ft, which stood at $1,868 psf in the latest quarter. Against the neighbours: The Sail @ Marina Bay averages $2,127 psf, V on Shenton $1,932 psf, One Shenton $1,879 psf, and the newer W Residences Marina View sits at $2,981 psf.

| Project | Tenure | Completed | Avg price (psf) |

|---|---|---|---|

| Marina One Residences | 99 yrs from 2011 | 2017 | $1,943 |

| W Residences Marina View | 99 yrs from 2021 | 2029 | $2,981 |

| The Sail @ Marina Bay | 99 yrs from 2002 | 2008 | $2,127 |

| V on Shenton | 99 yrs from 2011 | 2017 | $1,932 |

| One Shenton | 99 yrs from 2005 | 2011 | $1,879 |

So this was not a lone stumble in an otherwise firm project. Marina One’s average prices have declined around 21% since 2021, and the recent transaction record shows a cluster of one-bedders trading in the $1,240,000 to $1,330,000 range through April and May — $1,716 psf here, $1,740 psf there. The record low is the sharpest print in a soft patch, not a bolt from the blue.

And yet the fundamentals read well on paper. Completed in 2017, 99-year lease from July 2011 with about 84 years remaining. Within 800m of three MRT stations — Downtown, Marina Bay and Shenton Way. An estimated rental yield of 4.1% on 12-month average rents, with a relatively high 42% rentability. This is not a development the market has forgotten. It is a development the market has repriced.

Is a record low a floor or the first step down?

Here is the discipline I hold myself to, and it is worth stating plainly.

A single transaction is not a market.

Across five cycles, I’ve seen new lows that turned into floors — the print that, in hindsight, marked the moment sellers capitulated and value buyers stepped in. And I’ve seen new lows that turned into the first step down, the leading edge of a longer repricing. The honest answer at 2am is that we don’t know yet which one this is, and anyone who tells you they know from one transaction is selling you their confidence, not their analysis.

What actually tells you is the next two quarters of behaviour, not the last data point. I watch two things. First, volume: does the pace of resale transactions pick up at these levels, which suggests buyers see value, or does it thin out, which suggests sellers are still ahead of the market? Second, rental absorption: do units keep leasing quickly at holding rents? A 4.1% yield with 42% rentability is a real cushion — if that holds, the income story puts a practical floor under the capital story. If rents soften too, the repricing has further to run.

Why do CBD one-bedders behave differently from family homes?

This is the piece the headline cannot carry, and it is the most useful thing to understand about the Core Central Region.

A one-bedder in a 1,042-unit CBD development is close to a pure financial asset. Nobody raises children in it. There are no primary schools within a kilometre of Marina One — which matters not at all to its actual buyers, because its actual buyers are investors and its actual occupants are tenants: singles, couples, professionals on postings. That means its price is set by yield mathematics and investor sentiment, and both of those reprice fast. When interest rates, rental expectations or capital-flow moods shift, the CBD one-bedder market moves first and moves hardest.

A three-bedder in a family district trades on something stickier: school catchments, parents nearby, a decade of intended occupation. Owner-occupiers do not mark their homes to market every quarter, and they do not sell because sentiment turned. That is why the family segments move slower in both directions — and why reading the CCR through one product type is a category error.

The home that has to hold your family for ten years is rarely the home the headlines are reacting to this week.

So when a client sends me this headline and asks whether the market is falling, my first question back is: which market? The market for tenanted CBD one-bedders has clearly softened since 2021. The market for the homes most of my families actually live in is a different animal with different buyers, and it deserves its own evidence.

Should you be buying this dip?

For most of the families I work with — multi-generational households upgrading out of an HDB, or securing the next home in the S$1m to S$1.2m band — this news changes nothing. If anything it reinforces the discipline: the fact that a Marina Bay address with triple-MRT access can print a record low is a reminder that location prestige is not the same thing as price protection. Run the future-buyer test on any purchase: who buys this from you in fifteen years, and what will they be comparing it against? For a CBD one-bedder, the honest answer is another investor doing yield arithmetic — which is exactly why the entry price matters more than the address.

For investors, the arithmetic has genuinely improved. At $1,702 psf, the estimated 4.1% yield is doing real work, and the 21% decline since 2021 means the capital-loss risk is being priced in rather than ignored. But patience is the position. Which specific projects I’d watch, which I’d let pass, and at what levels — that depends on the next two quarters of volume and rental data, not this week’s print.

The quieter read — and I think the more interesting one — is for right-sizers.

The right-sizer question nobody is asking

Among the households I advise, there is a stage that arrives quietly: the landed home or large condo has done its job, the children have their own addresses, and two people are maintaining a house built for six. For that household, a compact CBD unit near three MRT lines, with low maintenance and the city at the doorstep, is not a consolation prize. It is a different shape of life.

A repricing like this one moves that conversation from abstract to concrete. A household sitting on landed equity can now weigh a Marina Bay pied-à-terre at levels below the district average, in a development whose build quality and gardens were never the problem. The question is not whether it is a discount. The question is the one I’d put on the table: will we still be glad we made the move smaller, sooner? If the answer is yes, the timing has rarely looked more sensible in this cycle. If the answer is uncertain, no psf figure resolves it.

That is the frame I’d bring to this headline for the families I serve: the record low is not an alarm and it is not an invitation. It is a reminder that the CBD prices like an asset class, that family homes price like homes, and that knowing which one you are buying — before you buy it — is most of the job. The rest of it, the project-by-project read, is what a conversation is for.

The numbers

| Sale price | S$1.3 million ($1,702 psf) |

| Unit | 764 sq ft one-bedroom, Marina One Residences |

| Seller's entry | April 2021 at $1,943 psf |

| Seller's outcome | Loss of $185,000 over ~5.1 years (-2.6% annualised) |

| Project average (12 months) | $1,943 psf |

| District 1 resale average | $1,868 psf (750–1,200 sq ft leasehold) |

| Tenure | 99 years from July 2011 (~84 years remaining) |

| Estimated rental yield | 4.1% |

Questions families ask

Is Marina One a good buy now that prices have hit a record low?

A record-low print is a data point, not a verdict. Marina One's average price has fallen about 21% since 2021, but the same development shows an estimated 4.1% rental yield and healthy rentability. Whether it suits you depends entirely on whether you are buying a tenanted asset, a right-sizing home, or a family home — and for the last of those, a CBD one-bedder was never the answer anyway.

Why are Marina One prices falling when it's in Marina Bay with three MRT stations nearby?

Location alone does not set price — the buyer pool does. CBD one-bedders trade in a thin resale pool dominated by investors, and that pool reprices quickly when yields, interest rates or rental demand shift. The development's fundamentals have not changed since 2021; the price its marginal buyer will pay has.

Does a low at Marina One mean CCR condos in general are falling?

No. A single transaction is not a market, and a one-bedder in a 1,042-unit CBD development is one of the most specific product types in Singapore. District 1's resale leasehold average sat at $1,868 psf in the latest quarter. If you want to read the CCR, watch volumes and rental absorption across projects over two quarters — not one print.

Who should actually be interested in a S$1.3 million CBD one-bedder?

Two profiles. Investors who buy on yield — at this entry price the estimated 4.1% rental yield and high rentability do the work, not capital-gain hopes. And right-sizers: a household sitting on landed or large-condo equity considering a compact, low-maintenance city home near transport. For a family that needs a ten-year home, it was never the product.

How long should you hold a CBD condo to avoid selling at a loss?

The Marina One seller held about five years and lost $185,000 — they bought at a strong point in the cycle and sold into a soft one. Holding period matters less than entry price relative to the cycle, but as a rule the CBD reprices harder and faster than family districts, so I'd want a horizon that can sit through a full cycle, not just a few years of it.

Reporting referenced: EdgeProp. Analysis and views are Adrian Lim's own.

Talking it through beats reading about it.

If this story touches a decision your family is weighing, send Adrian a message. A first conversation costs nothing and commits you to nothing.

WhatsApp Adrian · +65 8183 2333More from Insights

One Marina Gardens at $3,290 psf: What a Record High Really Signals

A new print at the top of District 1 is real news. It is also, for most Singapore families, scenery — and knowing the difference is worth more than the headline.

The S$2.93 Million Leonie Gardens Profit Took 28 Years. That's the Story.

Everyone is quoting the profit. Almost nobody is doing the division.

The Greater Southern Waterfront: Reading a 30km Story on Family Time

A 30-kilometre transformation is not one decision. It is several, on different clocks — and the clock that matters most is your family's.